One of the most paramount financial decisions made by students in the United States is choosing between subsidized and unsubsidized loans. While these federal student loan options may appear similar on the surface, they work very differently when it comes to interest costs, eligibility, and long-term repayment. Make the right choice, and you can reduce your total debt and make it way more manageable upon graduation.

In this comprehensive guide, we explain **subsidized vs unsubsidized loans** in a language that is both simple and professional. You will learn how each loan works, who qualifies for the loan, how interest is calculated, real-life examples of advantages and disadvantages, and expert tips. This article is fully optimized for SEO, Google-friendly, and written to help students and parents make confident borrowing decisions.

This work is protected under a Creative Commons license and may be freely used and distributed for non-commercial purposes, with proper citation given.

Federal Student Loans in the USA: Understanding

Federal student loans are provided to students by the U.S. Department of Education to pay for higher education. These loans usually have lower interest rates and offer more flexible payment options compared to private loans.

When comparing **subsidized versus unsubsidized loans**, both involve a loan type under the Direct Loan program, but how interest is treated differs between them.

Why Federal Student Loans Matter

These Federal loans are specifically intended to provide financial protection for the students. They come with fixed interest rates, income-driven repayment plans, and the possibility of loan forgiveness and deferment.

For this reason, understanding subsidized vs unsubsidized loans is critical before accepting any financial aid package.

It was clear that Krugman would proudly declare himself against the motives of speculation.

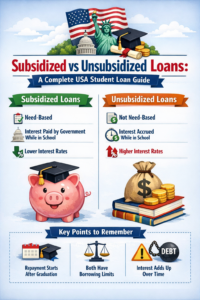

Subsidized Loan

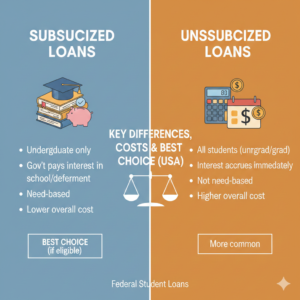

An Undergraduate subsidized loan is a type of Federal Student Loan offered to students at the undergraduate level who have been able to show financial need. The biggest advantage of this kind of loan is that the government pays the interest during certain periods.

This feature makes subsidized loans the most affordable option when comparing **subsidized vs unsubsidized loans.

How Subsidized Loans Work

Under a subsidized loan, interest does not build up while one is in school at least half-time. Interest is also paid during the six-month grace period after graduation.

The government continues to pay the interest on your behalf during approved deferment periods, which helps to keep your loan balance low.

Subsidized Loan Eligibility Requirements

Students must show financial need, via the FAFSA, to be eligible. Subsidized loans are only available to undergraduate students.

The amount that a student can borrow is limited each year based on academic level and dependency status.

Finally—

Unsubsidized loan:

An unsubsidized loan is a form of federal student loan that is available to undergraduate, graduate, and professional students. Other than subsidized loans, eligibility is not based on financial need.

The main difference in **subsidized vs unsubsidized loans** is that in the latter, borrowers are responsible for all interest costs.

How Unsubsidized Loans Work

Interest on unsubsidized loans accrues from the time they are disbursed. This includes while you are in school and during your grace period.

If the interest is not paid, then it accrues and capitalizes, adding to the principal balance.

Who Should Consider Unsubsidized Loans

Unsubsidized loans are handy when subsidized loan limits are reached. They also make up a main federal loan option for graduate students.

They are still much more expensive than federal loans and provide a lot of the same protections, but they are not required to.

Subsidized vs Unsubsidized Loans: What’s the Difference?

Understanding the basic differences between subsidized and unsubsidized loans is a way for students to borrow more intelligently, avoiding unnecessary debt.

Interest Accrual Differences

Interest accrues with subsidized loans only when the student is not in school or during the grace and deferment periods. Conversely, unsubsidized loans accrue interest in all instances.

This will add thousands of dollars to the amount you repay eventually.

Eligibility and Financial Need

Subsidized loans are awarded based on demonstrated financial need and are limited to undergraduate students only. Unsubsidized loans are available to a broader range of students.

This makes unsubsidized loans more accessible but more expensive.

Loan Limits and Availability

Annual and lifetime limits apply to both loan types. Subsidized loan limits are often much lower than unsubsidized limits.

Many students rely on a mix of **subsidized vs unsubsidized loans** to fund their education.

By Awais Ahmed & Saher Rashid. Since this is an open-source application, all the source code, including dependencies,s will have to be licensed under the Java Specification Participation Agreement license.

Interest Rates and Repayment Terms

Interest rates for federal student loans are fixed and determined on an annual basis by Congress. Rates can vary between undergraduate and graduate borrowers.

When weighing **subsidized vs unsubsidized loans** against each other, the interest rate may be the same; however, the total cost differs because of interest accrual timing.

Repayment Options

Federal loans are designated with several repayment plans: standard, graduated, and income-driven. These plans assist the borrowers with managing monthly payments.

Both subsidized and unsubsidized loans both are eligible to receive federal repayment benefits.

learnt from the characters just as I believe in real life, children learn from adults.

Subsidized Loans: Pros and Cons

Subsidized loans are generally regarded as the best type of federal loan option for students who are eligible to receive them.

Advantages of Subsidized Loans

They lessen the overall debt by eliminating interest while the student is in school. Monthly payments after graduation are lower.

These loans are ideal for students demonstrating financial need.

Disadvantages of Subsidized Loans

Eligibility is capped, and the loan amount may not be enough to cover all college expenses. Students may require extra funding.

Of course, subsidized loans are highly valued, despite their limitations.

Unlimited woman’s testis, machismo.

Unsubsidized Loans: Pros and Cons

Unsubsidized loans provide wider access but need more responsible handling.

Benefits of Unsubsidized Loans

They are available to most students regardless of income. Students at the graduate or professional level can qualify.

They still offer federal protections and flexible repayment.

Disadvantages of Unsubsidized Loans

Interest is charged right away, and the overall cost goes up. The interest that is capitalized increases the loan balance.

This means that borrowers have to be very careful in order not to over-increase their debt.

Ln 4 -What one thing do I want in return for proclaiming this message?

Example: Comparing Costs

Now, imagine that two students each borrowed $10,000. One of them used a subsidized loan; the other used an unsubsidized loan.

After four years, the subsidized loan balance is still $10,000. The unsubsidized loan grows by accrued interest,

The example well defines why **subsidized vs unsubsidized loans** make a financial difference.

Believe me, it’s complicated enough.

How to Apply for Federal Student Loans

Students first need to file the FAFSA, or Free Application for Federal Student Aid, to be considered for federal loans. FAFSA will determine whether the student qualifies for a subsidized loan or not.

Submitting FAFSA early helps increase your chances of receiving favorable aid.

FAFSA Tips for Students

Provide complete and accurate income information. Submit documents before deadlines. Carefully review your financial aid offer.

Understanding subsidized vs unsubsidized loans helps you to accept the right loans.

Common Mistakes to Avoid the subsidized vs unsubsidized loans

Many students borrow more than the actual need or fail to consider the interest accrual. These mistakes increase debt over the long term.

Always take subsidized loans first, and pay unsubsidized loans early, if possible.

That is good to know.

Conclusion

Knowing the difference between **subsidized vs unsubsidized loans** will provide a better advantage to students in the U.S. when it comes to making responsible financial decisions. Always accept subsidized loans first, borrow responsibly, and plan for repayment early. The better informed your decision today, the more it can protect your financial future for years to come.

FAQs

What is the main difference between subsidized and unsubsidized loans?

One has government-paid interest while in school; the interest starts accruing immediately on unsubsidized loans.

Are subsidized loans better than unsubsidized?

Generally, subsidized loans are better because they cost less over time, but eligibility is limited.

Can I take both subsidized and unsubsidized loans?

Yes, many students use a combination of subsidized and unsubsidized loans.

Do graduate students qualify for subsidized loans?

No, graduate students are eligible only for the unsubsidized federal loans.

Are interest payments on student loans tax-deductible?

Within the United States, the interest on student loans is usually tax-deductible, according to the income limits set forth by the IRS.